Text Book Back Questions and Answers - Chapter 9 Rectification of Errors 11th Accountancy Guide Samacheer Kalvi Solutions - SaraNextGen [2024-2025]

Updated On May 15, 2024

By SaraNextGen

Chapter 9 - Rectification of Errors - 11th Accounting Guide Samacheer Kalvi Solutions - Text Book Back Questions and Answers

Text Book Back Questions and Answers

I. Multiple Choice Questions

Choose the Correct Answer

Question 1.

Error of principle arises when ………………

(a) There is complete omission of a transaction

(b) There is partial omission of a transaction

(c) Distinction is not made between capital and revenue items

(d) There are wrong postings and wrong castings

Answer:

(c) Distinction is not made between capital and revenue items

Question 2.

Errors not affecting the agreement of trial balance are ………………

(a) Errors of principle

(b) Errors of overcasting

(c) Errors of undercasting

(d) Errors of partial omission

Answer:

(a) Errors of principle

Question 3.

The difference in trial balance is taken to ………………

(a) The capital account

(b) The trading account

(c) The suspense account

(d) The profit and loss account

Answer:

(c) The suspense account

Question 4.

A transaction not recorded at all is known as an error of ………………

(a) Principle

(b) Complete omission

(c) Partial omission

(d) Duplication

Answer:

(b) Complete omission

Question 5.

Wages paid for installation of machinery wrongly debited to wages account is an errs of ………………

(a) Partial omission

(b) Principle

(c) Complete omission

(d) Duplication

Answer:

(b) Principle

Question 6.

Which of the following errors will not affect the trial balance?

(a) Wrong balancing of an account

(b) Posting an amount in the wrong account but on the correct side

(c) Wrong totalling of an account

(d) Carried forward wrong amount in a ledger account

Answer:

(b) Posting an amount in the wrong account but on the correct side

Question 7.

Goods returned by Senguttuvan were taken into stock, but no entry was passed in the books. While rectifying this error, which of the following accounts should be debited?

(a) Senguttuvan account

(b) Sales returns account

(c) Returns outward account

(d) Purchases returns account

Answer:

(b) Sales returns account

Question 8.

A credit purchase of furniture from Athiyaman was debited to purchases account. Which of the following accounts should be debited while rectifying this error?

(a) Purchases account

(b) Athiyaman account

(c) Furniture account

(d) None of these

Answer:

(c) Furniture account

Question 9.

The total of purchases book was overcast. Which of the following accounts should be debited in the rectifying journal entry?

(a) Purchases account

(b) Suspense account

(c) Creditor account

(d) None of the above

Answer:

(b) Suspense account

Question 10.

Which of the following errors will be rectified using suspense account?

(a) Purchases returns book was undercast by 100

(b) Goods returned by Narendran was not recorded in the books

(c) Goods returned by Akila 900 was recorded in the sales returns book as 90

(d) A credit sale of goods to Ravivarman was not entered in the sales book

Answer:

(a) Purchases returns book was undercast by 100

II. Very Short Answer Questions

Question 1.

What is meant by the rectification of errors?

Answer:

Correction of errors in the books of accounts is not done by erasing, rewriting, or striking the figures which are incorrect. Correcting the errors that have occurred is called Rectification of errors.

Question 2.

What is meant by the error of principle?

Answer:

It means the mistake committed in the application of fundamental accounting principles in recording a transaction in the books of accounts.

Question 3.

What is meant by the error of partial omission?

Answer:

When the accountant has failed to record a part of the transaction, it is known as an error of partial omission. This error usually occurs in posting. This error affects only one account.

Question 4.

What is meant by the error of complete omission?

Answer:

It means the failure to record a transaction in the journal or subsidiary book or failure to post both the aspects in the ledger. This error affects two or more accounts.

Question 5.

What are compensating errors?

Answer:

The errors that make up for each other or neutralize each other are known as compensating errors. These errors may occur in related or unrelated accounts. Thus, excess debit or credit in one account may be compensated by excess credit or debit in some other account. These are also known as offsetting errors.

III. Short Answer Questions

Question 1.

Write a note on the error of principle by giving an example.

Answer:

It means the mistake committed in the application of fundamental accounting principles in recording a transaction in the books of accounts.

The following are the possibilities of error of principle:

1) Entering the purchase of an asset in the purchases book

Example: Machinery purchased on credit for ₹ 10,000 by M/s. Anbarasi garments manufacturing company entered in the purchases book.

2) Entering the sale of an asset in the sales book

Example: Sale of old furniture on credit for ₹ 500 was entered in the sales book.

3) Treating a capital expenditure as a revenue expenditure

Examples: An amount of ₹ 3,000 spent on the construction of an additional room is debited to the repairs account. Wages of ₹ 600 paid for the installation of a new machine are debited to the wages account.

4) Treating a revenue expenditure as a capital expenditure

Example: An amount of ₹ 2,000 paid for repairs to a machine is debited to the machinery account.

Question 2.

Write a note on the suspense account.

Answer:

When the trial balance does not tally, the amount of difference is placed to the debit (when the total of the credit column is higher than the debit column) or credit (when the total of the debit column is higher than the credit column) to a temporary account is known as ‘suspense account’.

Question 3.

What are the errors not disclosed by a trial balance?

Answer:

Certain errors will not affect the agreement of trial balance. Though such errors occur in the books of accounts, the total debit and credit balance will be the same. The trial balance will tally. Errors of complete omission, error of principle, compensating error, a wrong entry in the subsidiary books are not disclosed by the trial balance.

Examples of such errors are as follows:

- Treating revenue expenditure as capital expenditure

- Omitting a transaction completely

- Entering a transaction in a wrong subsidiary book

- Entering a transaction twice in a subsidiary book or journal

- Entering the amount of a transaction wrongly in the journal

- Entering the amount of transaction wrongly in the subsidiary book.

Question 4.

What are the errors disclosed by a trial balance?

Answer:

Certain errors affect the agreement of trial balance. If such errors have occurred in the books of accounts, the total of debit and credit balances will not be the same. The trial balance will not tally. The error of partial omission and error of commission affect the agreement of trial balance.

Question 5.

Write a note on one-sided errors and two-sided errors.

Answer:

- One-sided errors: When preparing the trial balance, if the total of debit balances and credit balances are not the same, there is a disagreement of the trial balance.

- Two-sided errors: Rectification of two-sided errors at the time of preparing the trial balance is just similar to that of their rectification before preparation of trial balance.

IV. Exercises

Question 1.

State the account/s affected in each of the following errors: (2 marks)

(a) Goods purchased on credit from Saranya for 150 were posted to the debit side of her account.

(b) The total of purchases book 4,500 was posted twice.

Answer:

(a) Purchases from Saranya should have been posted to the credit of Saranya’s A/c, but it has been debited. Hence, credit Saranya’s A/c with double the amount i.e., Rs. 300.

(b) Credit the Purchases A/c.

Question 2.

State the account/s affected in each of the following errors: (2 marks)

(a) Goods sold to Vasu on credit for 1,000 were not recorded in the sales book.

(b) The total sales book 2,500 was posted twice.

Answer:

(a)

(b) Debit the Sales A/c

Question 3.

Rectify the following errors discovered before the preparation of the trial balance: (2 marks)

(a) Sales book was undercast by 100

(b) Purchases returns book was overcast by 200

Answer:

(a) Sales account should be credited with 100

(b) Purchases returns account should be debited with 200

Question 4.

Rectify the following errors before the preparation of trial balance: (3 marks)

(a) Returns outward book was undercast by 2,000

(b) Returns inward book total was taken as 15,000 instead of 14,000

(c) The total of the purchases account was carried forward 100 less.

Answer:

(a) Returns outward Account should be credited with 2,000

(b) Sales returns account should be credited with 1,000

(c) Purchases account should be debited with 100

Question 5.

Rectify the following errors assuming that the trial balance is yet to be prepared: (5 marks)

(a) Sales book was undercast by 400

(b) Sales returns book was overcast by 500

(c) Purchases book was undercast by 600

(d) Purchases returns book was overcast by 700

(e) Bills receivable book was undercast by 800

Answer:

(a) Sales account should be credited with 400

(b) Sales returns account should be credited with 500

(c) Purchases account should be debited with 600

(d) Purchases returns account should be debited with 700

(e) Bills receivable account should be debited with 800

Question 6.

Rectify the following errors before preparing trial balance: (5 marks)

(a) The total of purchases book was carried forward 90 less.

(b) The total of purchases book was carried forward 180 more

(c) The total sales book was carried forward 270 less.

(d) The total of sales returns book was carried forward 360 more.

(e) The total of purchases returns book was carried forward 450 less.

Answer:

(a) Purchases account should be debited 90

(b) Purchases account should be credited 180

(c) Sales account should be credited 270

(d) Sales returns account should be credited with 360

(e) Purchases returns account should be credited with 450

Question 7.

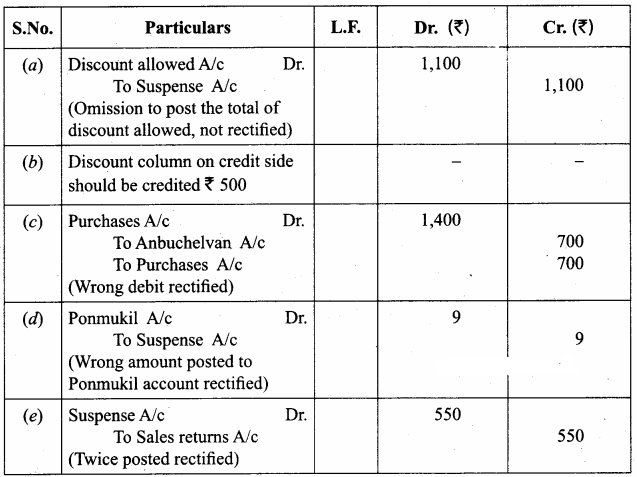

The following errors were located by the accountant before the preparation of the trial balance. Rectify them. (5 marks)

(a) The total of the discount column of 1,100 on the debit side of the cash book was not yet posted.

(b) The total of the discount column on the credit side of the cash book was undercast by 500.

(c) Purchased goods from Anbuchelvan on credit for 700 were posted to the debit side of his account.

(d) Sale of goods to Ponmukil on credit for 78 was posted to her account as 87.

(e) The total sales return book of 550 was posted twice.

Answer:

Question 8.

The accountant of a firm located the following errors before preparing the trial balance. Rectify them. (5 marks)

(a) Machinery purchased for 3,000 was debited to the purchase account.

(b) Interest received 200 was credited to the commission account.

(c) An amount of 1,000 paid to Tamilselvan as salary was debited to his personal account.

(d) Old furniture sold for 300 was credited to the sales account.

(e) Goods worth 800 purchased from Soundarapandian on credit were not recorded in the books of accounts.

Answer:

Rectifying Journal

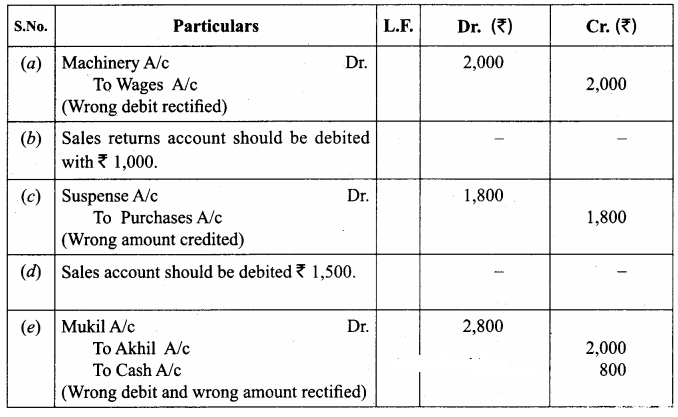

Question 9.

Rectify the following errors which were located before preparing the trial balance. (5 marks)

(a) Wages paid 2,000 for the erection of machinery was debited to wages account.

(b) Sales returns book was short totaled by 1,000.

(c) Goods purchased for 200 were posted as 2,000 to the purchases account.

(d) The sales book was overcast by 1,500.

(e) Cash paid to Mukul ₹ 2,800 which was debited to Akhil’s account as ₹ 2,000.

Answer:

Rectifying Journal

Question 10.

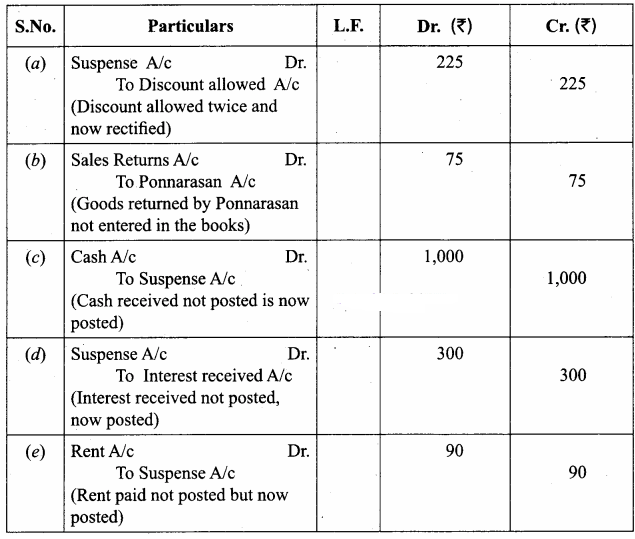

Rectify the following errors which were located at the time of preparing the trial balance: (5 marks)

(a) The total of the discount column on the debit side of the cash book of 225 was posted twice.

(b) Goods of the value of 75 returned by Ponnarasan were not posted to his account.

(c) Cash received from Yazhini 1,000 was not posted.

(d) Interest received 300 has not been posted.

(e) Rent paid 100 was posted to rent account as 10.

Answer:

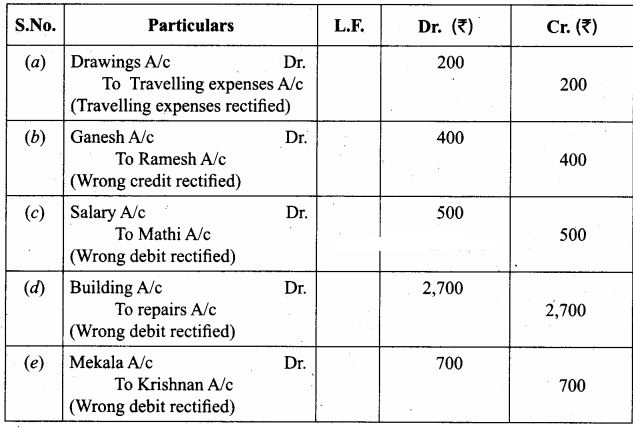

Question 11.

The following errors were located at the time of preparing the trial balance. Rectify them. (5 marks)

(a) A personal expense of the proprietor 200 was debited to travelling expenses account.

(b) Goods of 400 purchased from Ramesh on credit were wrongly credited to Ganesh’s account.

(c) An amount of 500 paid as salaries to Mathi was debited to his personal account.

(d) An amount of 2,700 paid for the extension of the building was debited to the repairs account.

(e) A credit sale of goods of 700 on credit to Mekala was posted to Krishnan’s account.

Answer:

Question 12.

Rectify the following journal entries. (5 marks)

Answer:

Question 13.

Rectify the following errors discovered after the preparation of the trial balance: (5 marks)

(a) Rent paid was carried forward to the next page 500 short.

(b) Wages paid were carried forward 250 excess.

Answer:

(a) Rent account is to be debited with 500.

(b) Wages account is to be credited with 250.

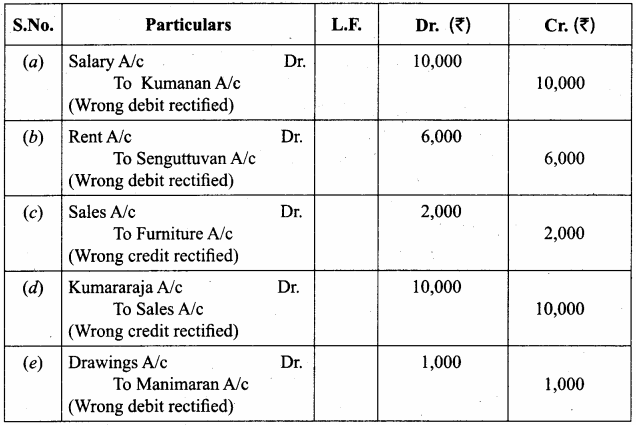

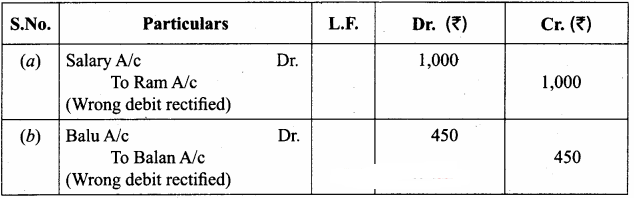

Question 14.

Rectify the following errors after preparation of trial balance: (5 marks)

(a) Salary paid to Ram ₹ 1,000 was wrongly debited to his personal account.

(b) A credit sale of goods to Balu for 450 was debited to Balan.

Answer:

Question 15.

Pass necessary journal entries to rectify the following errors located after the preparation of trial balance: (5 marks)

(a) Sales book was undercast by 1,000.

(b) An amount of 500 paid for wages was wrongly posted to the machinery Account.

Answer:

(a) Sales account should be credited 1,000.

(b)

Question 16.

Give journal entries to rectify the following errors discovered after the preparation of trial balance: (5 marks)

(a) Purchases book was overcast by 10,000.

(b) Repairs to the furniture of 500 were debited to the furniture account.

(c) A credit sale of goods to Akilnilavan for 456 was credited to his account as 654.

Answer:

(a) Purchases account should be credited 10,000.

Question 17.

Rectify the following errors located after the preparation of trial balance: (5 marks)

(a) Purchases book was undercast by 900.

(b) Sale of old furniture for 1,000 was credited to sales account.

(c) Purchase of goods from Arul for 1,500 on credit was not recorded in the books.

Answer:

(a) Purchases account should be debited with 900.

Question 18.

The following errors were located after the preparation of trial balance. Pass journal entries to rectify them. Assume that there exists a suspense account. (5 marks)

(a) The total of sales book was undercast by 350.

(b) The total of the discount column on the debit side of cash book 420 was not posted.

(c) The total of one page of the purchases book of 5,353 was carried forward to the next page as 5,533.

(d) Salaries 2,400 was posted as 24,000.

(e) Purchase of goods from Sembiyanmadevi on credit for 180 was posted to her account as 1,800.

Answer:

Rectifying Journals

Question 19.

Rectify the following errors assuming that the trial balance is already prepared and the difference was placed to suspense account: (5 marks)

(a) Sales book was undercast by 250.

(b) Purchases book was undercast by 120.

(c) Sales book was overcast by 130.

(d) Bills receivable book was undercast by 75.

(e) Purchases book was overcast by 35.

Answer:

(a) Sales account should be credited 250.

(b) Purchases account should be debited 120.

(c) Sales account should be debited 130.

(d) Bills receivable account should be debited 75.

(e) Purchases account should be credited 35.

Question 20.

The following errors were located after the preparation of the trial balance. The difference in trial balance has been taken to the suspense account. Rectify them. (5 marks)

(a) The total of purchases book was carried forward 70 less.

(b) The total sales book was carried forward 340 more.

(c) The total of purchases book was carried forward 150 more.

(d) The total sales book was carried forward 200 less.

(e) The total of purchases returns book was carried forward 350 less.

Answer:

Rectifying Journals

Question 21.

The following errors were located by the accountant after the preparation of the trial balance. There exists a suspense account. Rectify them. (5 marks)

(a) The total of the discount column of 1,180 on the debit side of the cash book was not posted.

(b) Purchase of goods from Arivuchelvan on credit for 600 was posted to the debit side of his account.

(c) The total of the discount column on the credit side of the cash book was undercast by 400.

(d) The total sales returns book of 570 was posted twice.

(e) Sold goods to Mukil on credit for 87 was posted to her account as 78.

Answer:

Question 22.

The accountant of a firm located the following errors after preparing the trial balance. Rectify them assuming that there is a suspense account. (5 marks)

(a) Machinery purchased for 3,500 was debited to the purchase account.

(b) 1,800 paid to Raina as salary was debited to his personal account.

(c) Interest received 200 was credited to the commission account.

(d) Goods worth 1,800 purchased from Amudhanila on credit was not recorded in the books of accounts.

(e) Used furniture sold for 350 was credited to the sales account.

Answer:

Question 23.

The bookkeeper of a firm found that the trial balance was out by 922 (excess credit). He placed the amount in the suspense account and subsequently found the following errors: (5 marks)

(a) The total discount column on the credit side of the cash book 78 was not posted in the ledger.

(b) The total of purchases book was short by 1,000.

(c) A credit sale of goods to Natarajan for 375 was entered in the sales book as 735.

(d) A credit sale of goods to Mekala for 700 was entered in the purchases book. You are required to give rectification entries and prepare a suspense account.

Answer:

Suspense Account

Question 24.

The books of Raman did not agree. The accountant placed the difference of 1,270 to the debit of the suspense account. Rectify the following errors and prepare the suspense account:

(a) Goods took by the proprietor for his personal use 75 was not entered in the books.

(b) A credit sale of goods to Shanmugam for 430 was credited to his account as 340.

(c) A purchase of goods on credit for 400 from Vivek was entered in the sales book. However, Vivek’s account was correctly credited.

(d) The total of the purchases returns book 300 was not posted.

Answer:

Suspense Account

Textbook Case Study Solved

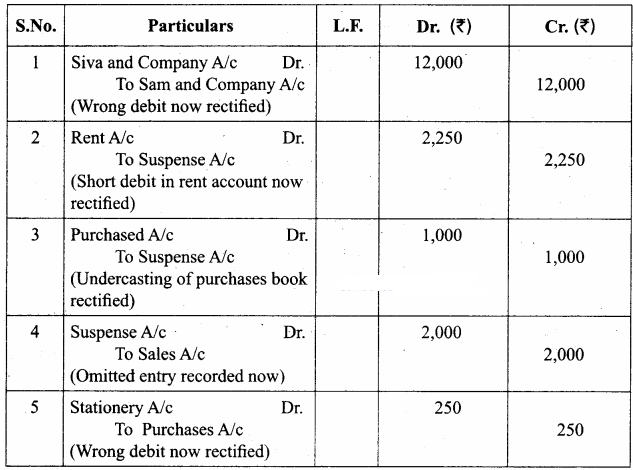

Question 1.

Rameela, a class 11 student, visited one of her relative’s furniture shops. She met the accountant of the shop. He was busy preparing final accounts. At that time, one of the staff approached the accountant with a list of errors found in ledger postings. Rameela asked the accountant, in a surprised tone, “Is it possible to rectify the errors before preparing the final accounts?” The accountant replied, “Yes, it is!” final accounts?” The accountant replied,

“Yes, it is!”

Rameela was curious to analyze the errors. She found the following:

- Furniture sold on credit to Siva and company for 12,000 was debited to Sam and company;

- Rent paid 2,500, was debited to rent account as 250.

- The total purchase journal was undercast by 1,000.

- A sales invoice for 2,000, completely omitted from the books.

- Stationery bought for 250, was posted to purchases account.

Can you help Rameela to identify and rectify the errors?

Answer:

Additional Questions and Answers

I. Multiple Choice Questions

Choose the correct answer

Question 1.

Goods of 5, 000 purchased from Mr.B were recorded in sales book, the rectification of this error will ________.

a) Increase the gross profit

b) Reduce the gross profit

c) Have no effect on gross profit

d) None of the above

Answer:

b) Reduce the gross profit

Question 2.

When the accountant has failed to record a part of the transaction is known as ………………

(a) Error of partial omission

(b) Error of commission

(c) Compensating errors

(d) Error of principle

Answer:

(a) Error of partial omission

Question 3.

Goods worth 500 given as charity should be credited to ________.

a) Charity Account

b) Sales Account

c) Purchases Account

d) None of the above

Answer:

c) Purchases Account

Question 4.

The total salary account is carried forward ₹ 1200 excess ……………….

(a) Errors in carrying forward

(b) Errors in posting

(c) Errors in casting

(d) Errors of commission

Answer:

(a) Errors in carrying forward

Question 5.

________ are those transactions which are not recorded as per the rules of debit and credit.

a) Error of principle

b) Error of Commission

c) Error of Omission

d) Compensating errors

Answer:

a) Error of principle

II. Very Short Answer Questions

Question 1.

What do you mean by error?

Answer:

The error means recording or classifying or summarizing the accounting transactions wrongly or omissions to record them by a clerk or an accountant unintentionally.

Question 2.

What is an error of commission?

Answer:

When a transaction is incorrectly recorded, it is known as an error of commission. It usually occurs due to lack of concentration or carelessness of the accountant.

Question 3.

What do you meaning by errors?

Answer:

An error means recording or classifying or summarising the accounting transactions wrongly or omissions to record them by a clerk or an accountant unintentionally.

III. Short Answer Questions

Question 1.

What are the types of errors at the stage of journalizing?

Answer:

- Error of omission

- Error of commission

- Error of principle

Question 2.

What are the types of errors at the stage of posting?

Answer:

(i) Errors of Omission:

- The error of complete omission

- The error of partial omission

(ii) Errors of Commission:

- Posting to the wrong account

- Posting of wrong account

- Posting to the wrong side

Question 3.

What are the types of errors at the stage of preparing a trial balance?

Answer:

(i) Error of Omission

(ii) Error of Commission:

(a) Entering to the wrong account

(b) Entering the wrong amount

(c) Entering to the wrong side of trial balance, etc.

Also Read : Text-Book-Back-Questions-and-Answers-Chapter-10-Depreciation-Accounting-11th-Accountancy-Guide-Samacheer-Kalvi-Solutions